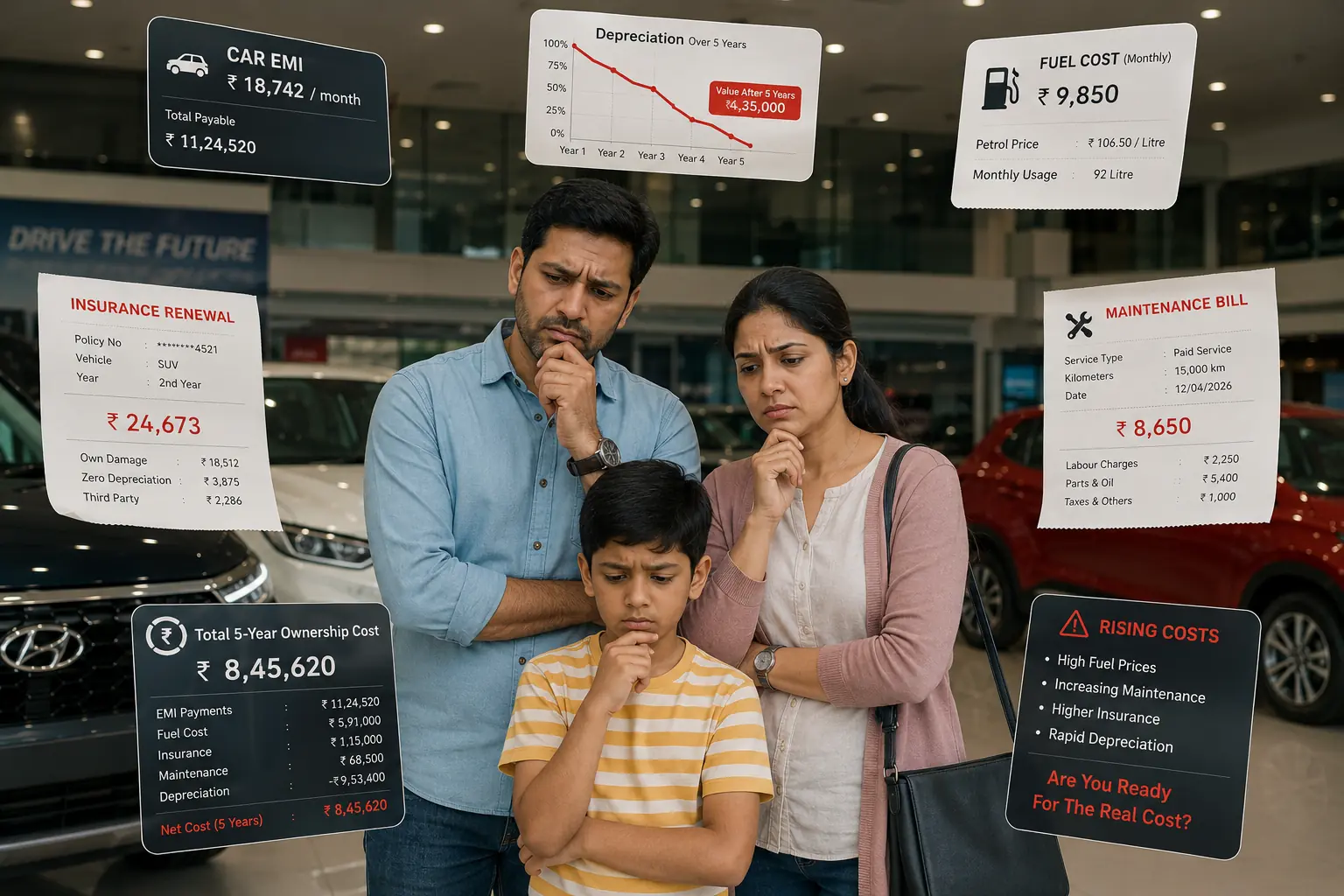

Most car buyers in India make the same costly mistake, they judge affordability only by the EMI. But the true total cost of car ownership in India goes far beyond your monthly loan payment and fuel bill. From insurance renewals and rising maintenance costs to depreciation that quietly eats away your car’s value, the real expense is often 30%–40% higher than what buyers initially expect. Understanding these hidden costs is the difference between a smart purchase and a long-term financial burden.

What most buyers underestimate before purchasing a car

The true cost of owning a car in India goes far beyond the EMI and fuel bill. Expenses like insurance renewals, depreciation, maintenance, parking, tolls, and loan interest quietly increase your monthly outflow by 25% to 35%. A car that “fits your EMI budget” can still strain your finances if these hidden costs are ignored.

Cost of car Ownership in India: Beyond Just Fuel and EMI

Walk into almost any dealership in India, and the first question is usually:

“Sir, what EMI are you comfortable with?”

That sounds convenient, but it’s one of the biggest financial traps in car buying.

A car isn’t just a one-time purchase or a monthly EMI. It’s an ongoing financial commitment that continues long after you leave the showroom. Between fuel bills, insurance renewals, servicing, tire replacements, tolls, parking fees, and depreciation, the real ownership cost is often far higher than buyers initially expect.

This is why smart buyers focus on the Total Cost of Ownership (TCO) instead of just the showroom price.

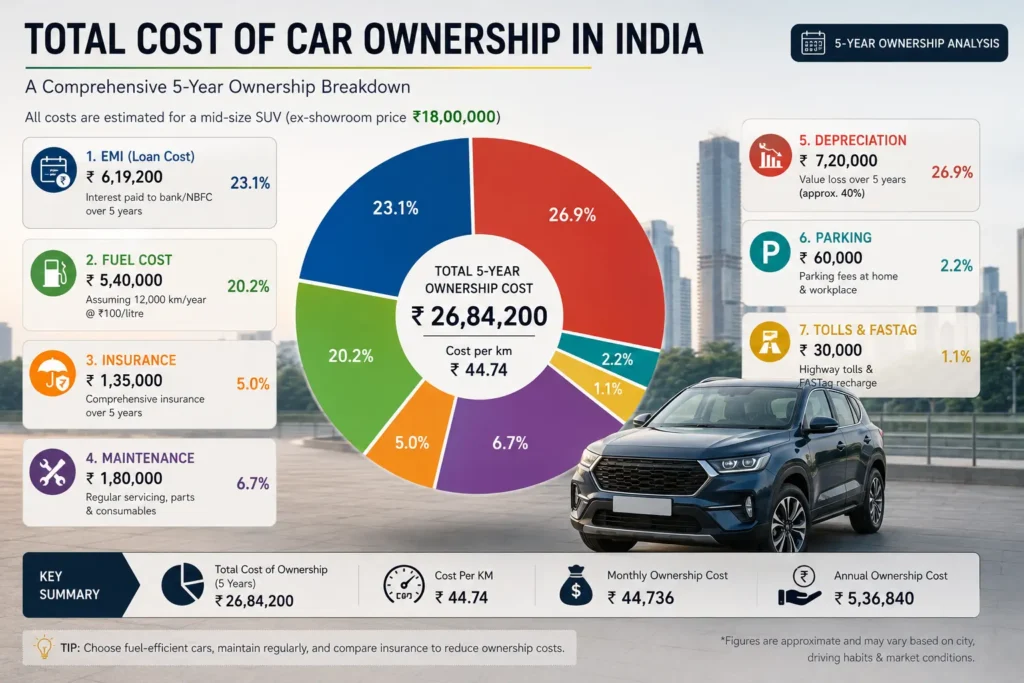

1. What Is the Total Cost of Ownership (TCO)?

Total Cost of Ownership (TCO) is the complete amount you spend on a car during the entire period you own it. It includes the purchase cost, loan interest, fuel, insurance, maintenance, parking, tolls, and depreciation minus the resale value.

In simple words:

TCO = Every rupee your car takes from your pocket over time.

For example:

- You buy a car for ₹10 lakh

- Spend ₹5 lakh on fuel and maintenance over 5 years

- Pay ₹2 lakh in loan interest and insurance

- Sell the car for ₹5 lakh

Your actual ownership cost isn’t ₹10 lakh — it’s closer to ₹12 lakh after adjusting for resale value.

Why TCO Matters

Most buyers compare:

- EMI

- Mileage

- Features

Very few calculate:

- Long-term maintenance

- Depreciation losses

- Running costs

- Interest burden

That’s where budgeting mistakes begin.

2. Why EMI Is Only Part of the Story

EMI only repays the loan. It does not include fuel, maintenance, insurance, parking, tolls, or depreciation.

This is why two people paying the same EMI can experience completely different financial pressure depending on how much they drive and maintain the car.

The Long-Tenure Trap

Many buyers choose:

- 6-year loans

- 7-year loans

- low down payments

because it reduces the EMI.

But longer tenure means:

- more total interest,

- higher insurance exposure,

- slower equity buildup,

- and higher overall ownership cost.

Example: ₹8 Lakh Loan at 9%

| Tenure | EMI | Total Interest |

|---|---|---|

| 4 Years | Lower overall cost | ~₹1.5 Lakh |

| 7 Years | Lower EMI | ~₹2.8 Lakh |

A “comfortable EMI” often hides a massive long-term interest burden.

3. Fuel Costs Over 5 Years

Fuel becomes one of the largest recurring ownership expenses, especially for Indian commuters driving daily in city traffic.

For someone driving:

- 1,000–1,200 km/month

- with petrol around ₹100+/liter

fuel spending alone can cross several lakhs within five years.

Estimated 5-Year Fuel Cost

| Vehicle Type | Avg Mileage | Approx 5-Year Fuel Cost |

|---|---|---|

| Petrol Hatchback | 15 km/l | ₹4–₹5 Lakh |

| Diesel SUV | 18 km/l | ₹3–₹4 Lakh |

| Hybrid Car | 24 km/l | ₹2–₹3 Lakh |

Choosing the right fuel type also plays a huge role in long-term ownership cost, especially when comparing maintenance, resale value, and yearly running distance. If you’re confused about fuel choice in 2026, read our detailed guide on diesel vs petrol ownership cost in India to understand which option makes better financial sense for your driving pattern.

Why Fuel Costs Rise Faster Than Expected

- traffic congestion,

- AC usage,

- rising fuel prices,

- aggressive driving habits,

- poor maintenance.

In cities like Bengaluru, Mumbai, and Delhi, stop-go traffic significantly reduces real-world mileage compared to claimed ARAI figures.

Most buyers discover that why real mileage is lower than ARAI mileage claims, especially in heavy Indian traffic and daily AC usage conditions.

4. Insurance Costs Most Buyers Ignore

Insurance is not a one-time expense. It is an annual recurring cost that continues throughout ownership.

Most buyers only notice the first-year insurance bundled into the on-road price.

But renewals continue every year.

Hidden Insurance Costs

- Zero-dep cover renewals

- Engine protection add-ons

- Return-to-invoice cover

- Flood protection in metro cities

- Rising third-party premiums

Typical Annual Insurance Costs

| Vehicle Segment | Annual Premium |

|---|---|

| Hatchback | ₹12,000–₹18,000 |

| Sedan | ₹18,000–₹28,000 |

| SUV | ₹25,000–₹45,000 |

Luxury vehicles can easily cross ₹1 lakh annually.

5. Maintenance and Service Expenses

Modern cars are cheaper to maintain early on, but ownership costs rise significantly after warranty periods end.

Most buyers only calculate scheduled service cost.

But real maintenance includes:

- tires,

- batteries,

- brake pads,

- suspension,

- clutch wear,

- AC repairs,

- wheel alignment,

- unexpected breakdowns.

Typical Ownership Timeline

| Year | Common Expenses |

|---|---|

| 1–2 | Basic servicing |

| 3–4 | Battery replacement |

| 4–5 | Tire replacement |

| 5+ | Suspension, clutch, AC work |

Hidden Maintenance Reality

A single unexpected repair can cost:

- ₹20,000 to ₹80,000+

especially in:

- turbo petrol cars,

- diesel SUVs,

- luxury vehicles.

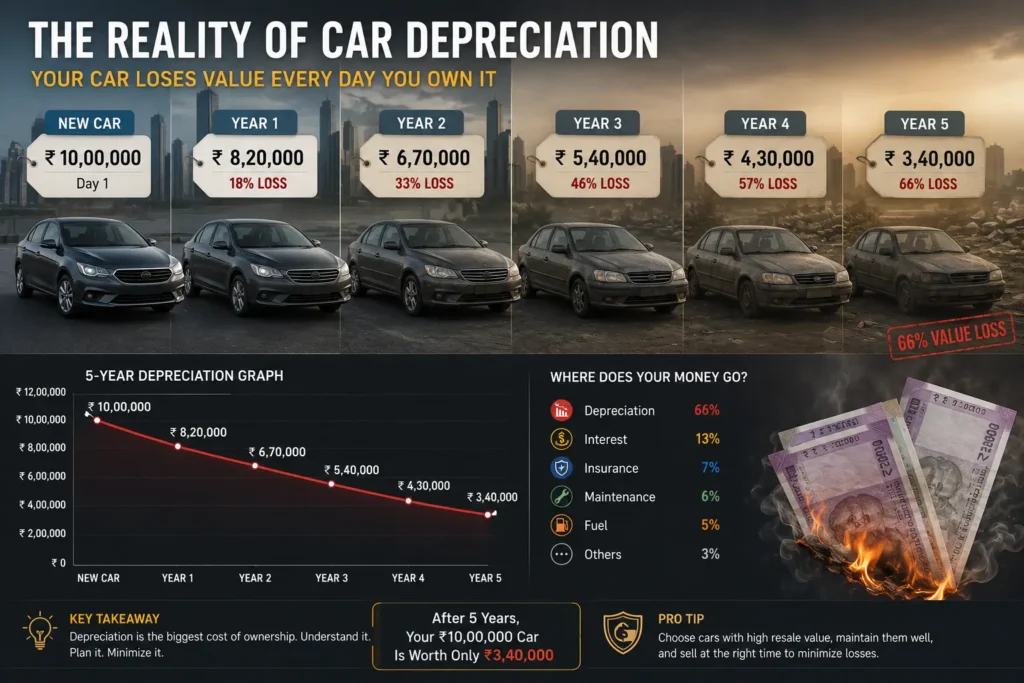

6. Depreciation: The Biggest Hidden Expense

Depreciation is the reduction in your car’s market value over time, and it is usually the single largest ownership expense.

The moment a new car leaves the showroom, it loses value.

Typical Depreciation in India

| Ownership Year | Approx Value Retained |

|---|---|

| Year 1 | 80–85% |

| Year 3 | 65–70% |

| Year 5 | 50–55% |

Example

A ₹12 lakh SUV may only sell for:

- ₹6–₹7 lakh after five years.

That means:

- ₹5 lakh+ vanished through depreciation alone.

Cars With Better Resale Value

Brands that usually retain value better:

- Maruti Suzuki

- Toyota

- Honda

Cars with weaker resale:

- niche brands,

- luxury sedans,

- discontinued models.

7. Parking, Tolls, and Daily Usage Costs

Daily usage expenses quietly add thousands to your monthly ownership cost.

These include:

- parking fees,

- FASTag recharge,

- washing,

- accessories,

- traffic fines,

- society parking charges.

Common Monthly Expenses in Metro Cities

| Expense | Approx Monthly Cost |

|---|---|

| Parking | ₹1,000–₹4,000 |

| Tolls/FASTag | ₹500–₹3,000 |

| Car Cleaning | ₹500–₹1,500 |

| Accessories & Misc. | ₹500–₹2,000 |

For urban commuters, these “small” expenses become significant over time.

8. Comparing Hatchback vs SUV Ownership Cost

Estimated Monthly Ownership Comparison

| Expense Item | Hatchback (₹6L) | Compact SUV (₹12L) |

|---|---|---|

| EMI | ₹10,500 | ₹21,000 |

| Fuel | ₹6,000 | ₹8,500 |

| Insurance | ₹1,200 | ₹2,800 |

| Maintenance | ₹800 | ₹1,500 |

| Parking/Tolls | ₹1,000 | ₹2,000 |

| Total Monthly Cost | ₹19,500 | ₹35,800 |

The Reality

A buyer planning only for the EMI might think:

- ₹21k/month.

Actual ownership reality:

- closer to ₹36k/month.

That gap causes financial stress for many families.

9. The Psychological Mistake Most Buyers Make

Buyers often mistake “loan approval” for “affordability.”

Banks approve loans based on:

- income,

- credit score,

- repayment capacity.

But that does not mean the car comfortably fits your lifestyle.

Common Emotional Buying Mistakes

- buying bigger SUVs for status,

- stretching budget for sunroof/features,

- ignoring future fuel costs,

- underestimating maintenance,

- focusing only on monthly EMI.

Many first-time buyers underestimate how quickly hidden ownership costs accumulate beyond the showroom price and EMI. This detailed breakdown of the hidden costs of buying a car in India explains how fuel, insurance, depreciation, maintenance, and loan interest quietly increase your real monthly expenses.

This creates:

- investment delays,

- reduced savings,

- emergency fund pressure,

- “car-poor” lifestyle.

10. How to Calculate Real Car Affordability

Your total car expenses should ideally remain within 10–15% of your monthly take-home salary.

Practical Budget Rule

If your salary is:

- ₹1 lakh/month

then total ownership cost should stay around:

- ₹10k–₹15k/month ideally,

- ₹20k max for comfort.

Smart Ownership Planning Checklist

Before buying:

- Calculate total monthly cost

- Keep emergency savings intact

- Avoid zero-down-payment loans

- Compare insurance outside dealership

- Estimate 5-year fuel expense

- Research resale value

11. Ways to Reduce Total Ownership Cost

Smart Strategies That Actually Work

- Choose fuel-efficient vehicles

- Prefer shorter loan tenure

- Increase down payment

- Compare insurance annually

- Avoid unnecessary accessories

- Maintain tire pressure properly

- Service car on time

- Drive smoothly to reduce wear

Simple driving habit changes can significantly reduce monthly fuel spending and improve real-world mileage over time. Explore these practical ways to improve fuel efficiency to lower fuel costs and get better mileage in daily Indian driving conditions.

The Biggest Saver

Buying the “right-sized” car usually saves more money than chasing luxury features.

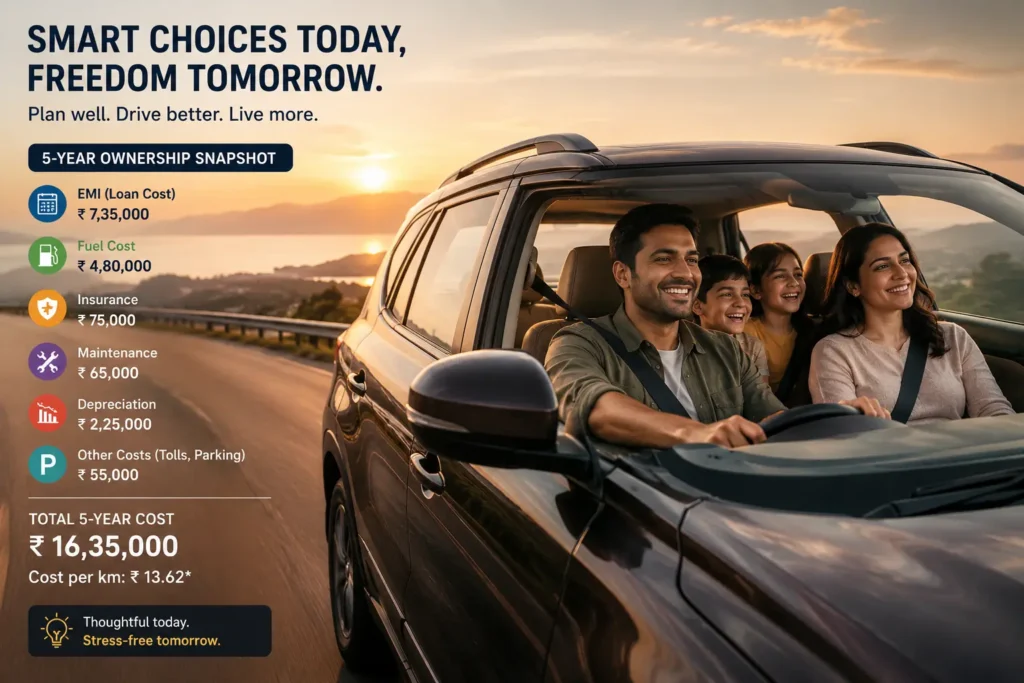

12. Is Car Ownership Worth It Financially?

Editorial Perspective: Strictly financially, a car is a depreciating asset. But real life is not just spreadsheets.

For Indian families, a car offers:

- convenience,

- safety,

- emergency mobility,

- travel flexibility,

- comfort during extreme weather.

The key is not avoiding car ownership.

The key is:

owning a car that supports your lifestyle without damaging your long-term finances.

Questions Buyers Commonly Ask Before Purchasing a Car

What is the total cost of ownership?

It includes all expenses related to owning a car:

- EMI,

- fuel,

- maintenance,

- insurance,

- depreciation,

- parking,

- tolls,

- and repairs.

Is EMI the biggest car expense?

Not always. Over time, fuel and depreciation can cost more than the EMI interest itself.

How much does a car cost monthly in India?

For most middle-class buyers:

- hatchbacks: ₹15k–₹20k/month,

- compact SUVs: ₹25k–₹40k/month.

What hidden expenses do car owners forget?

Most commonly:

- insurance renewal,

- tire replacement,

- battery replacement,

- parking fees,

- FASTag recharge,

- depreciation loss.

Is buying a car financially smart?

It can be — if ownership costs comfortably fit within your budget and do not interrupt your savings or investments.

Looking Beyond the Showroom Price

A car doesn’t become expensive when you buy it.

It becomes expensive slowly:

- at the fuel pump,

- during insurance renewal,

- inside service centers,

- and when resale value drops every year.

The smartest buyers are not the ones buying the most expensive car.

They are the ones who understand the full financial picture before signing the papers.

One Last Thought Before You Buy

A car should improve your life — not quietly consume your salary month after month.

Plan for the hidden costs today, and your ownership experience will feel rewarding instead of stressful.

The Bottom Line (Quick Summary)

The true cost of car ownership includes much more than EMI and fuel expenses. Indian car buyers must also budget for insurance renewals, maintenance, tire replacement, parking, tolls, loan interest, and depreciation. These hidden costs can increase total monthly ownership expenses by 25–35%, making Total Cost of Ownership (TCO) essential for realistic financial planning.

Helpful Resources

🏦 Reserve Bank of India (RBI)

Official regulator for banking rules, lending policies, and interest rate guidelines in India.

👉 https://www.rbi.org.in/

📊 TransUnion CIBIL

Check your credit score and understand how it impacts loan approval and interest rates.

👉 https://www.cibil.com/

🚗 SBI Auto Loans

Compare car loan options, interest rates, and eligibility from India’s largest public sector bank.

👉 https://sbi.co.in/web/personal-banking/loans/auto-loans

🏦 HDFC Bank Car Loans

Explore flexible financing options for new and used cars with private banking benefits.

👉 https://www.hdfc.bank.in/car-loan

🚘 ICICI Bank Vehicle Finance

Find competitive car loan plans, EMI calculators, and eligibility details.

👉 https://www.icicibank.com/personal-banking/loans/car-loan

Also Read: Diesel vs Petrol Cars: Which Makes Financial Sense in 2026?

Disclaimer: The figures and estimates mentioned in this article are for informational purposes only and may vary based on location, vehicle type, and market conditions.