So, you’re ready to bring home that new set of wheels? Whether it’s a sleek EV or a rugged SUV, the excitement is real. But before you get lost in the “new car smell,” let’s talk about the one thing that can turn a dream purchase into a financial headache: the lowest car loan interest rate.

In 2026, the car loan market in India has shifted. With the RBI holding the repo rate steady at 5.25% as of mid-year, banks are competing hard for your business. But here’s the secret: the “starting at” rate you see on a billboard isn’t what everyone gets. The lowest rates are reserved for the “smart borrowers” who know how to play the game.

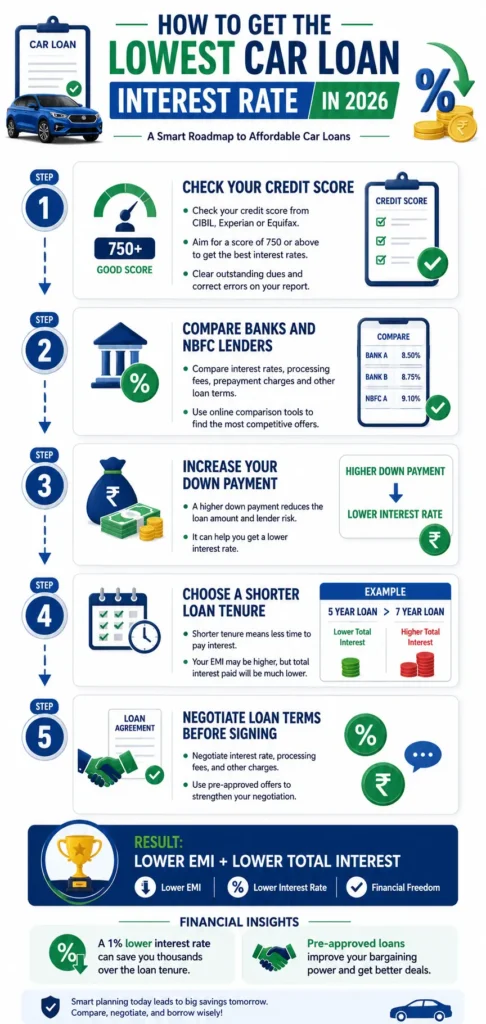

If you don’t want to leave money on the table, here are five proven strategies to secure the lowest car loan interest rate today.

TL;DR: How to Pay Less for Your Car

- Boost your CIBIL: Aim for 750+ to unlock the best rates (often starting around 7.60%).

- Shop beyond the dealer: Compare public sector banks (PSUs) against private lenders.

- Increase your down payment: Aim for 20% to reduce the lender’s risk and your rate.

- Keep it short: Shorter tenures (3–5 years) usually have lower rates than 7-year plans.

- Negotiate: Always ask for a processing fee waiver and check for “Green Loan” discounts for EVs.

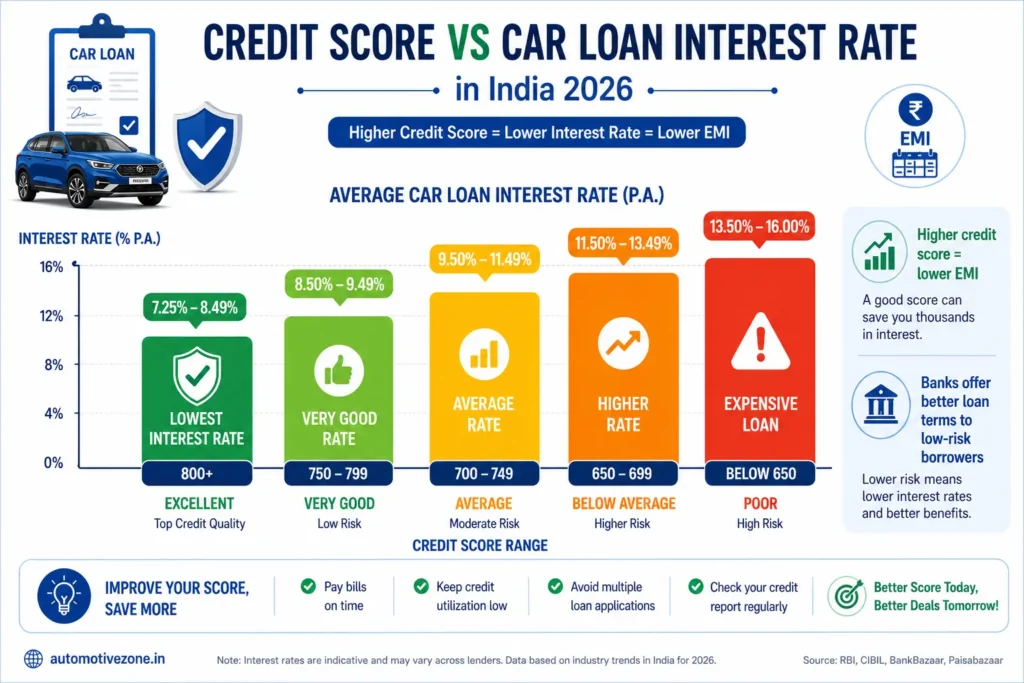

1. Polish Your Credit Score (The 750+ Rule)

Think of your credit score as your financial resume. In 2026, banks use “risk-based pricing.” This means if your CIBIL score is 800, you might get a rate of 7.65%, but if it’s 650, you could be staring at 10.50%.

On a ₹8 lakh loan over 5 years, that 3% difference is roughly ₹65,000 extra out of your pocket.

Tip: Check your credit report at least 60 days before applying. If there’s an error or a tiny unpaid credit card bill, fix it now. Bringing your score above the 750 mark is the fastest way to slash your Car Loan Interest Rate.

2. Master the Art of the Down Payment

Many lenders today offer “Zero Down Payment” or “100% On-Road Funding.” It sounds tempting, doesn’t it? But it’s a trap.

When you take 100% funding, the bank sees more risk. To compensate, they charge a higher interest rate. By putting down at least 20-25% of the on-road price, you show the bank you have “skin in the game.” This often lets you negotiate a rate that is 0.25% to 0.50% lower than the standard offer.

While planning your down payment and EMI structure, it’s also important to understand how loan decisions affect your overall long-term budget. Many buyers underestimate the full financial impact, which is explained in cost of car ownership in India beyond EMI.

3. Compare PSUs vs. Private Banks vs. NBFCs

Your car dealer will likely push their “preferred partner” bank. Why? Because they often get a commission. While convenient, the dealer’s rate is rarely the lowest.

| Lender Type | Typical Interest Rate (2026) | Best For |

| Public Sector Banks (SBI, BoB) | 7.60% – 8.80% | Lowest rates, low processing fees |

| Private Banks (HDFC, ICICI) | 8.25% – 9.50% | Speed, digital processing, pre-approved offers |

| NBFCs (Bajaj, Mahindra) | 9.50% – 12.00% | Flexibility for lower credit scores |

Start with a Public Sector Bank like SBI or Bank of Baroda. Their car loan eligibility criteria might be stricter, but their rates are almost always the benchmark for “lowest.”

However, loan interest is only one part of the total expense. Real ownership costs also include fuel, maintenance, insurance, and depreciation. You can explore the complete breakdown in true cost of car ownership hidden expenses India.

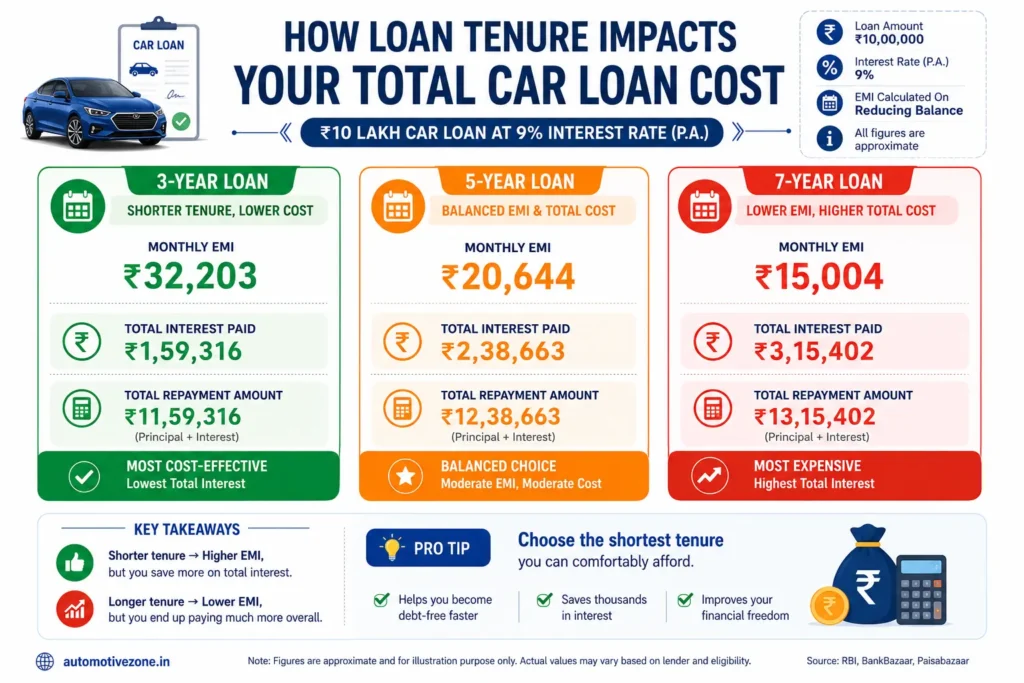

4. Choose Your Tenure Wisely

A 7-year loan (84 months) makes your car loan EMI look incredibly small and affordable. But there’s a catch. Longer tenures often come with slightly higher interest rates, and you end up paying significantly more in total interest.

For example, on a ₹10 lakh loan at 8.5%:

- 5-Year Tenure: Total interest paid is ~$2.3$ lakhs.

- 7-Year Tenure: Total interest paid is ~$3.3$ lakhs.

You’re paying an extra ₹1 lakh just for the “comfort” of a lower monthly payment. If you can afford the higher EMI, stick to a 3-to-5-year window.

Your monthly EMI decisions should also consider how fuel efficiency impacts long-term running costs. Even a small difference in mileage can significantly affect your budget, as explained in ARAI mileage vs real mileage India.

5. Negotiate the Hidden Costs

The interest rate isn’t the only cost. Look out for:

- Processing Fees: These can range from ₹3,000 to 1% of the loan. In 2026, most banks will waive this if you have a good relationship with them or apply during a festive season.

- Fixed vs. Floating: A fixed rate stays the same, while a floating rate changes with the RBI repo rate. In a stable or falling interest rate environment (like early 2026), a floating rate can actually save you money over time.

Common Mistakes to Avoid

- Ignoring the “On-Road” vs. “Ex-Showroom” Difference: Ensure your loan covers registration and insurance if you aren’t paying those upfront.

- Falling for “Low EMI” Schemes: Always look at the Annualized Percentage Rate (APR). Some “low EMI” deals have balloon payments at the end that can sting.

- Not Disclosing Existing Debts: If you have too many active personal loans, your car loan eligibility drops, and the bank might hike the rate to cover their risk.

Real-World Example: The “Chai-Coffee” Savings

Let’s say you’re taking a ₹7 lakh loan.

- Bank A offers 9.0%

- Bank B (after you negotiated) offers 8.2%

That 0.8% difference saves you roughly ₹950 per month. Over 5 years, that’s ₹57,000. That is enough to pay for your car’s periodic servicing for the next three years!

Frequently Asked Questions About Car Loan Interest Rates

What credit score is needed for the lowest car loan interest rate?

In 2026, a CIBIL score of 750 or above is generally required to qualify for the lowest advertised interest rates (typically around 7.60%–8.00%).

Can I negotiate my car loan interest rate?

Yes. If you have a long-standing relationship with a bank or a high salary, you can negotiate the rate. Often, showing a competitor’s quote is the best leverage.

Is a longer tenure better for a car loan?

Only for monthly cash flow. A longer tenure reduces your EMI but significantly increases the total interest you pay over the life of the loan.

Which banks offer the lowest car loan interest rates in India?

Currently, Public Sector Banks like State Bank of India (SBI), Bank of Baroda, and Union Bank offer the most competitive rates, often starting below 8%.

Does a down payment reduce car loan interest?

Yes. A higher down payment (20%+) reduces the loan-to-value (LTV) ratio, making you a “safer” borrower, which can lead to a lower interest rate offer.

Getting the lowest car loan isn’t about luck; it’s about preparation. By keeping your credit score high, comparing at least three different lenders, and opting for the shortest tenure you can comfortably afford, you can save tens of thousands of rupees.

Before you sign that loan agreement, take ten minutes to run your numbers through a car loan EMI calculator. A little bit of math today can lead to a lot of freedom tomorrow.

Ready to start? Compare the latest car loan offers from top banks today and see how much you can save on your next drive!